KRNN Return Predictor & Scalable Data Engineering

The Method: I engineered a K-parallel GRU encoder (KRNN) trained via Gaussian Negative Log-Likelihood to output next-day return $\mu$ and volatility $\sigma$. By mean-pooling across $K$ independent GRUs, I aimed to reduce the variance in the network's predictions.

The Math: The network optimizes the per-sample GNLL loss:

$$ \mathcal{L}(\mu,\sigma;y) = \frac{1}{2} \log(\sigma^2) + \frac{(y-\mu)^2}{2\sigma^2} $$

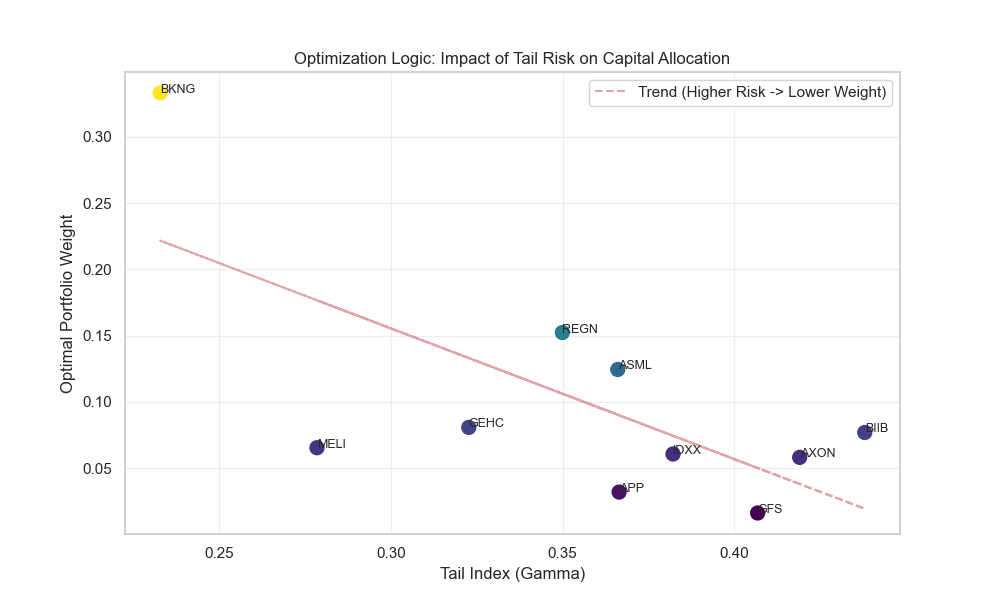

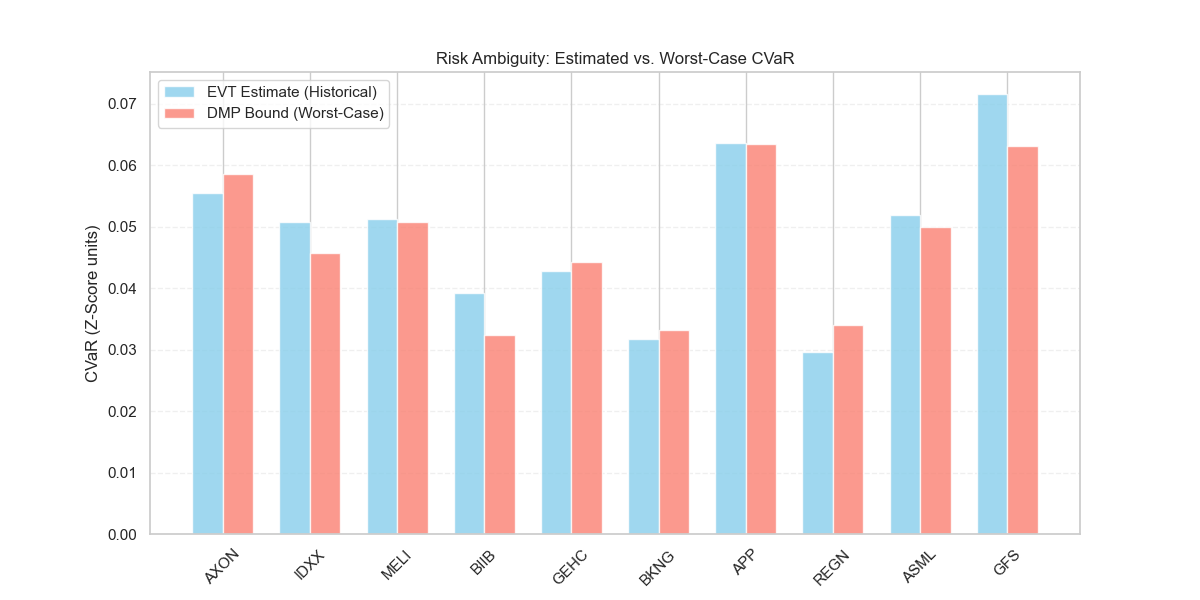

Engineering & Reality: To ensure code scalability and avoid "quiet" data leaks, I built a modular PyTorch pipeline utilizing Parquet for I/O efficiency, strictly separating the StandardScaler fit to the training chronologies. While the predictive alpha proved negligible ($R^{2} \approx 0$), isolating the standardized residuals ($Z_t$) provided the exact heteroscedastic signals needed for the downstream tail-risk engines.